People are still falling for these scams in 2026, and the numbers are alarming. Ponzi vs pyramid scheme remains one of the most searched financial crime topics worldwide precisely because the traps keep working dressed in new language, promoted through new platforms, but running on the same basic deception that has been stealing people’s savings for over a century.

Understanding the difference between the two, knowing where they came from, and recognizing the warning signs before money changes hands is not just useful for millions of people in developing economies where financial literacy remains limited, it is genuinely protective. This is what you need to know.

Background: What Is a Ponzi Scheme?

The Ponzi meaning has a very specific origin, and knowing it helps explain why the term has stuck so firmly in the global financial vocabulary.

The name comes from Charles Ponzi, an Italian-born fraudster who became one of the early 20th century’s most notorious financial criminals. He did not invent the concept of paying old investors with new investors’ money — that trick is older than he was — but he ran it at a scale and with a confidence that made his name synonymous with the method forever after.

In a Ponzi scheme, the fundamental structure is straightforward: early investors receive payments that appear to be returns on their investment. In reality, those payments are funded entirely by money coming in from newer investors. No actual profit is being generated. The whole thing is a closed loop that only keeps moving as long as new money keeps arriving and it always eventually stops arriving.

For anyone wondering about the Ponzi pronunciation, it is simply “Pon-zee.” And today, the Ponzi meaning extends well beyond the original case it is the standard term for any investment fraud that works by recycling new investor money to pay earlier ones.

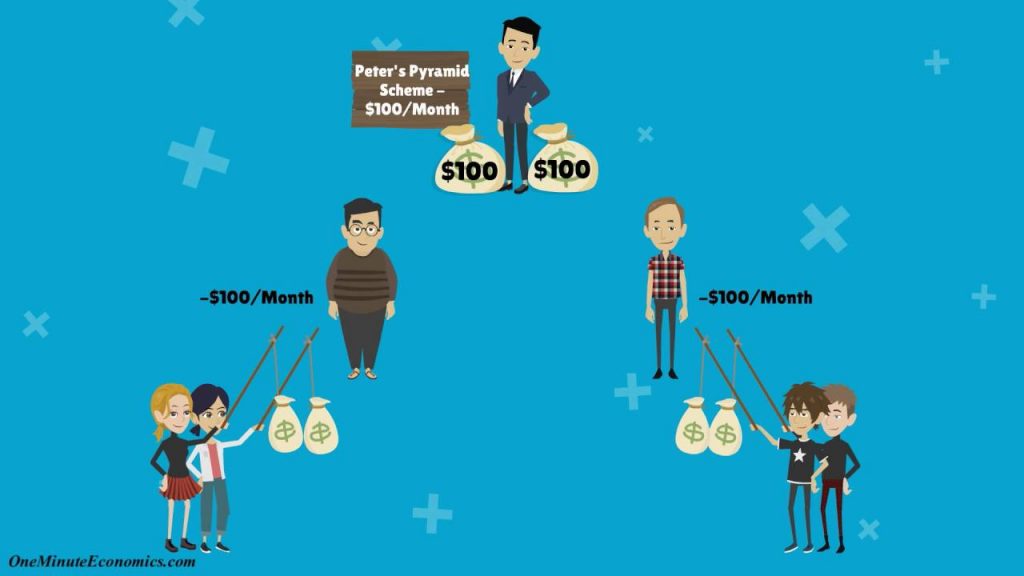

Ponzi vs Pyramid Scheme: Key Difference

This is where a lot of people get confused, and the confusion is understandable both are frauds, both eventually collapse, and both leave victims with significant losses. But the mechanics are different in ways that matter.

In a Ponzi scheme, most victims do not know they are participating in a fraud at all. They believe they have invested in a legitimate business or fund, and for a while, the returns they receive reinforce that belief. The deception is centralized the fraudster at the center manages everything and keeps up the illusion.

A pyramid scheme works differently. Participants are typically asked to recruit new members, and their earnings depend directly on how many people they bring in and how many people those recruits bring in. The structure fans out in layers which is where the pyramid shape comes from. Early participants at the top can do well. The overwhelming majority of participants toward the base of the pyramid lose money, because the recruitment chains cannot expand forever.

Despite these differences, Ponzi vs pyramid scheme comparisons almost always end in the same place: both models are mathematically guaranteed to collapse. The only question is when, and who is left holding the losses when they do.

Charles Ponzi and the Origin of the Scam

Charles Ponzi’s story is one of the more remarkable in the history of financial crime not because what he did was technically sophisticated, but because of the sheer audacity with which he pulled it off and the scale he reached before anyone stopped him.

In the early 1920s, Ponzi built his scheme around international postal reply coupons a genuinely obscure financial instrument that most of his investors did not understand and did not particularly try to. He promised extraordinary returns within a short timeframe, and in the early days, those promises appeared to be kept. Word spread. Money poured in.

The reality, of course, was that he was paying early investors with the deposits of newer ones, spending lavishly on himself along the way, and maintaining the illusion with enough confidence to stay ahead of scrutiny for longer than anyone should have allowed. When the scheme finally collapsed, the losses were substantial and the damage to financial trust in Boston’s investment community lasted for years.

His name became the permanent label for this type of fraud the Ponzi meaning model and it has been applied to cases on every continent in the century since.

Bernie Madoff: The Largest Ponzi Scheme in History

If Charles Ponzi was the man who gave the fraud its name, Bernie Madoff is the man who took it to a scale that seemed almost impossible to believe even after it was exposed.

Madoff ran his investment firm for decades, consistently delivering steady and attractive returns to a client list that included wealthy individuals, charities, hedge funds, and institutional investors. His reputation was impeccable. His firm was well-established. The returns were not outlandish enough to trigger obvious suspicion which, in retrospect, was part of the genius of the deception.

When the 2008 financial crisis hit and clients began requesting large-scale withdrawals simultaneously, the entire structure collapsed almost overnight. What investigators found underneath was staggering a Ponzi scheme that had been running for years, possibly decades, with no actual investment activity generating the reported returns. Billions of dollars were simply gone.

The Bernie Madoff case is now a mandatory reference in any serious discussion of financial fraud. It is studied in business schools, regulatory agencies, and journalism programs as the definitive modern example of how completely a well-onstructed deception can fool sophisticated, educated, financially experienced people when the fraudster is skilled enough and lucky enough to keep new money coming in.

Ponzi Scheme in Movies and Pop Culture

The Ponzi scheme movie genre has quietly become its own category in documentary and dramatic filmmaking, and for good reason these stories have everything that makes for compelling narrative. Trust built over years. Warning signs ignored. The moment of collapse. The search for answers among victims who still cannot fully believe what happened to them.

Hollywood and streaming platforms have found that fraud stories resonate with broad audiences because they tap into something universal the fear of being deceived, the desire for financial security, and the uncomfortable recognition that clever, charming people can run successful con operations for a very long time if the social and regulatory conditions allow it.

Beyond entertainment, the Ponzi scheme movie format has become a genuine educational tool. Awareness campaigns in multiple countries have used documentary-style presentations of real cases to help ordinary investors recognize warning signs they might otherwise miss.

Double Shah Case in Pakistan

For anyone tempted to think that Ponzi vs pyramid scheme fraud is primarily a Western problem, the Double Shah case in Pakistan offers a sharp corrective.

Double Shah operating in Khairpur attracted investors from across Sindh with promises of dramatic returns that defied any rational explanation grounded in legitimate investment. The returns he claimed to offer were simply not achievable through any real business activity, but for investors who were drawn in by early payments and social proof, the warning signs were not obvious enough to stop the money flowing.

When the scheme eventually collapsed, the losses were widespread and deeply felt in communities that could least afford them. Legal proceedings followed, but recovering money once it has been absorbed into a Ponzi-style structure is notoriously difficult.

The Double Shah case established itself as the reference point in Pakistan for discussions of financial fraud, and it is still cited by the SECP and financial literacy advocates when explaining why skepticism about guaranteed high returns is not paranoia — it is common sense.

SECP Warnings and Financial Awareness

The Securities and Exchange Commission of Pakistan has been increasingly active in warning the public about illegal investment schemes, and the patterns it describes are consistent with what fraud analysts observe globally.

Social media has become one of the primary recruitment channels for these schemes in Pakistan and across the region. Platforms that allow targeted outreach to specific communities, combined with the social credibility that comes from being recommended by someone you trust, have made it easier than ever to spread fraudulent investment opportunities faster than regulatory agencies can respond.

The SECP’s consistent message is worth repeating: any investment that promises fixed high returns with no meaningful risk is not a legitimate opportunity. Markets do not work that way. Returns that sound too good to be true are, without exception, either fraudulent or unsustainably structured — which amounts to the same thing when the collapse eventually comes.

Understanding Ponzi meaning and the mechanics of pyramid schemes before engaging with any unfamiliar investment opportunity remains the most reliable protection available to ordinary investors.

Global Impact of Ponzi Schemes

The damage done by Ponzi vs pyramid scheme fraud across the world is not measured only in the direct financial losses, though those are enormous — in the billions of dollars across documented cases in the United States, Europe, South Asia, Southeast Asia, and beyond.

The deeper damage is to trust. When a financial fraud is exposed particularly one that involved people who were trusted community members, respected figures, or apparently credible institutions — the ripple effects extend far beyond the direct victims. People who were not involved become more reluctant to participate in legitimate investment activity. Financial systems lose credibility. The environment for economic development becomes more difficult.

In countries with weaker regulatory enforcement, these effects are compounded. Frauds that might be detected earlier in more tightly supervised markets can run for years, drawing in more victims and causing more damage before the collapse becomes visible.

Financial education is increasingly being recognized not as a nice-to-have supplement to regulatory oversight, but as a primary defense that has to be built at the individual level because no regulatory system can catch every fraudster before they cause harm.

Conclusion

The Ponzi vs pyramid scheme distinction is worth understanding, but the more important lesson is the one that sits underneath both categories: financial fraud works by exploiting trust, promising returns that cannot be legitimately generated, and sustaining the illusion long enough to take as much money as possible before the collapse that was always coming finally arrives.

From Charles Ponzi’s postal coupon scheme in 1920s Boston to Bernie Madoff’s decades-long operation in New York, from Double Shah’s community-based fraud in Khairpur to the social media schemes the SECP is warning about today the core trick has not changed. Only the delivery mechanism has.

Knowing the Ponzi meaning, understanding how pyramid structures work, and applying genuine skepticism to any opportunity that promises guaranteed high returns are not sophisticated financial concepts. They are basic protective tools that are available to anyone willing to learn them — and learning them before engaging with an unfamiliar investment is almost always considerably less painful than learning about them afterward.

FAQs

How much debt does Pakistan owe?

Pakistan’s total debt is a figure that changes regularly as a result of new borrowing, IMF program disbursements, currency fluctuations, and repayments on existing obligations. It includes both domestic debt money owed to institutions and investors within Pakistan and external debt owed to international creditors. The exact figure at any given moment is tracked by the State Bank of Pakistan and international institutions including the IMF and World Bank, and is part of ongoing discussions about Pakistan’s fiscal sustainability and economic management. For current numbers, official government and IMF sources provide the most reliable data.

What is the number one poorest country?

There is no permanently fixed answer to this question because rankings shift as economies grow, contract, and are affected by conflict or political instability. Countries including South Sudan, Burundi, and the Central African Republic have frequently appeared near the bottom of GDP per capita rankings in recent years, largely due to ongoing armed conflict, political dysfunction, and limited access to the resources and infrastructure needed for economic development. Any current ranking should be checked against the latest World Bank or IMF data, as conditions can change significantly within a short period.

Is Pakistan a first, second, or third world country?

The first, second, and third world framework is a Cold War-era classification system that most economists and development specialists consider outdated and no longer useful for describing modern economic conditions. It was originally based on political alignment rather than economic development. In contemporary usage, Pakistan is generally classified as a developing country or an emerging economy, based on indicators including GDP per capita, human development index scores, industrialization levels, and access to public services. Within that category, it sits in a middle range more developed than some of its neighbors, less developed than others.